Monthly Financial To-Do List

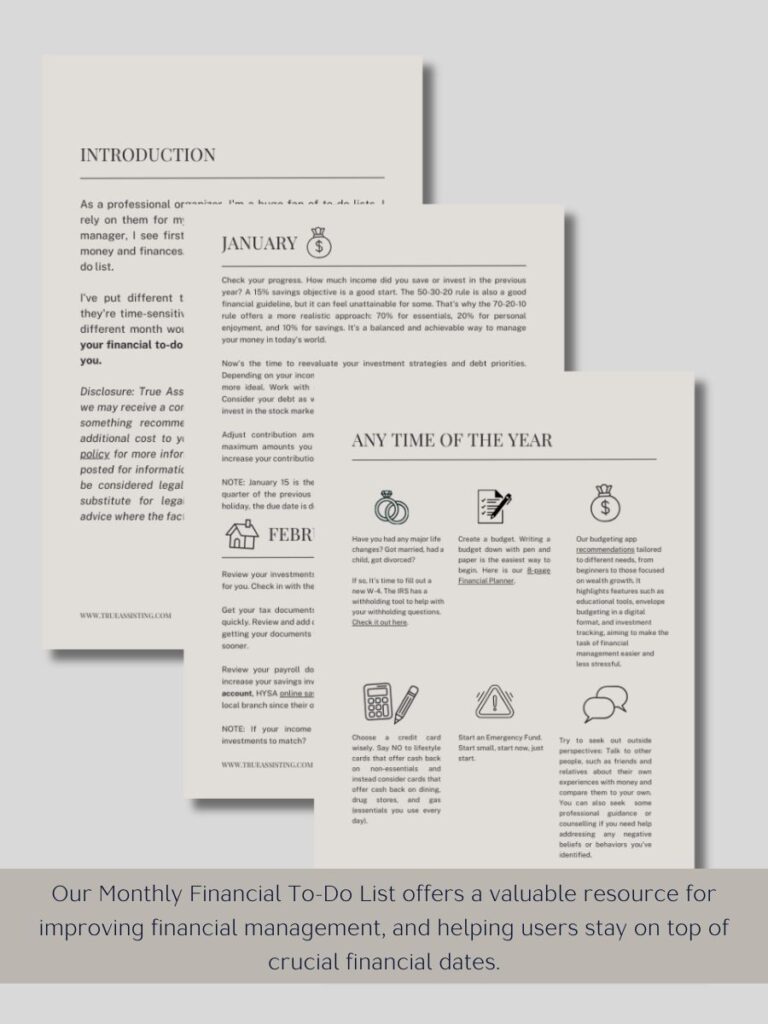

Unlock financial clarity with our Monthly Financial To-Do List! Designed to streamline your money management, this comprehensive to-do ensures you never miss an important date, helps you track your savings, and provides actionable tips to optimize your spending. Whether you’re a finance novice or a budgeting pro, this guide is your roadmap to financial peace of mind. Subscribe now and take the guesswork out of your monthly finances!

To download this free guide, please sign up with the form below and you will be sent an email with your download link.